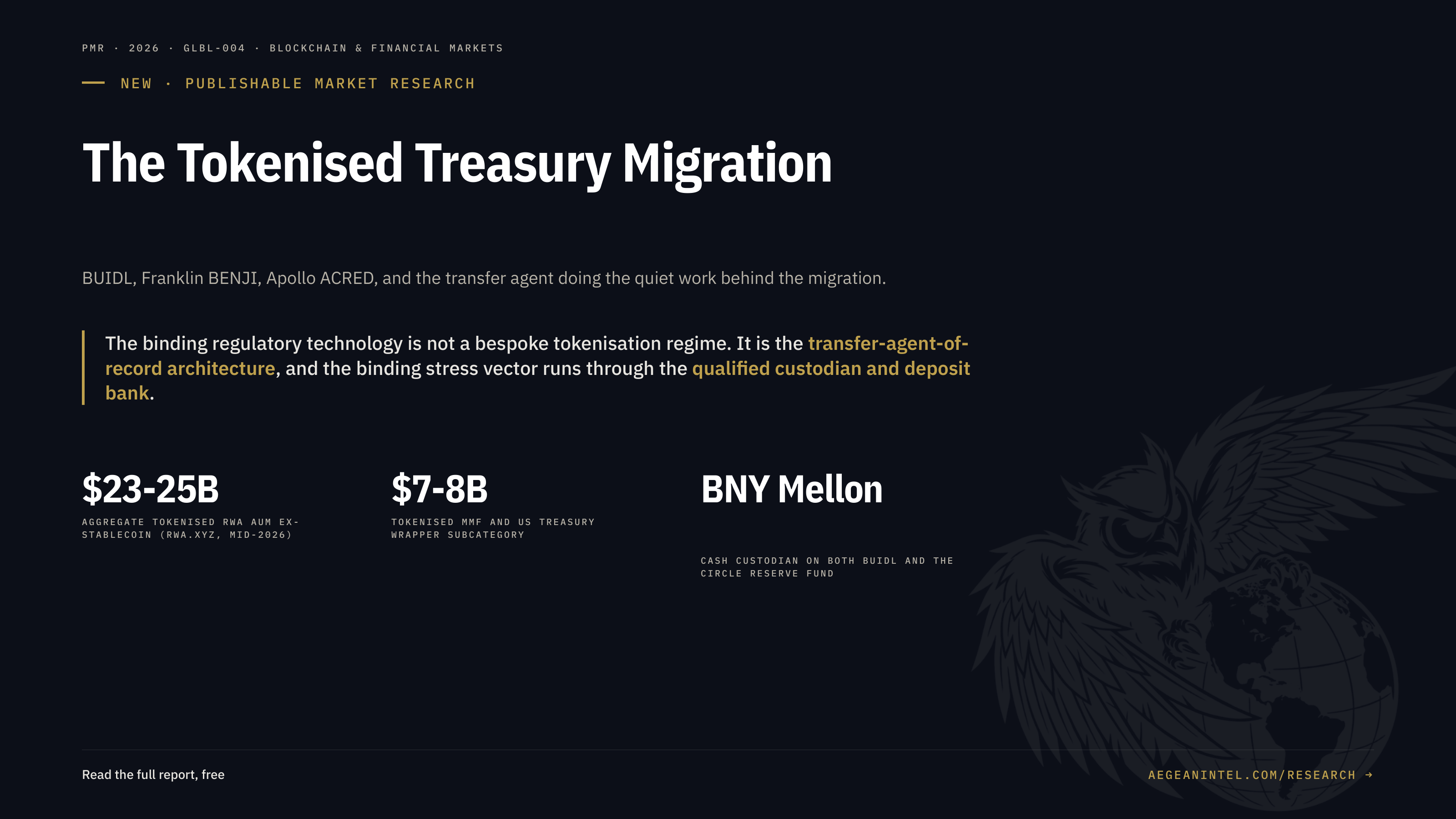

Tokenised money-market funds, US Treasury wrappers, and private-credit access vehicles have moved from pilot to material institutional scale across 2024 through mid-2026. The binding regulatory technology that enabled the transition is not a bespoke tokenisation regime; it is the transfer-agent-of-record architecture that lets blockchain records function as an operational mirror while the transfer agent retains the authoritative book of record. The binding adoption driver is operational, not yield. The binding stress vector runs through the qualified-custodian and deposit-bank channel, the same architecture flagged in our companion stablecoin piece.

Read the full PMR (PDF) →Key Judgments

The assessment turns on three load-bearing judgments. Each is tied to cited evidence in the body of the brief and carries an explicit confidence level.

- High confidence. Tokenised RWAs have crossed from pilot to material institutional scale: USD 23 to 25 billion aggregate AUM (ex-stablecoin), USD 7 to 8 billion in the tokenised-MMF and Treasury subcategory, with BUIDL, FOBXX, OUSG, USDY, ACRED, and SCOPE forming an identifiable institutional cohort.

- High confidence. The binding adoption driver is operational, not yield. The yield delta on the MMF wrapper is approximately zero against the traditional equivalent; what moves the allocation is 24/7 settlement, atomic composability with stablecoin reserves (the BUIDL to USDC redemption rail), and regulated secondary access for previously illiquid private-credit feeders.

- High confidence. The binding stress vector runs through the qualified-custodian and deposit-bank channel. BNY Mellon serves as cash custodian on both BUIDL and the Circle Reserve Fund, replicating the single-counterparty concentration finding from the companion stablecoin piece.

- Moderate confidence. Statutory progress (OCC NPR finalisation, BUIDL and BENJI confirmed as eligible stablecoin reserve assets) drives aggregate AUM to USD 35 to 50 billion by mid-2027 under baseline; the deterioration scenario looks closer to March 2023 USDC than to UST 2022.